Why Retail Investors Spend Years Learning to Buy and Never Learn to Sell

Most Retail investors treat the entry as the decision and the exit as something that will figure itself out. It never does.

If you have spent any time learning about investing — through YouTube, courses, books, through conversations with people who sound like they know , you have noticed something. Almost everything is about buying.

When to buy, what to buy and at what price to buy. Which screener to use, which ratio to check, which sector is undervalued and which stock is a “multibagger in the making.”

The entire education system around retail investing is designed for entry. The language is about entry. The excitement is about entry. The screenshots are about entry.

Now think about the last time you saw someone teach selling with the same seriousness. Not a stop-loss number. Not “book profits at 20 percent.” An actual philosophy for when and why to leave a position , one that accounts for what the business is doing, what has changed, what your money now needs to do, and what your emotions are telling you versus what the situation actually requires.

That education barely exists. And that gap is where a large share of investor damage quietly accumulates.

The imbalance is not accidental

The reason entry gets all the attention is not a mystery. Entry is exciting. It carries hope. It is the moment of commitment, of possibility, of imagining where a stock could go. The brain rewards the act of buying because it registers as progress , you made a decision, you deployed capital, you are now “in the market.”

Selling carries none of that. Selling is a verdict. It says: this is done. Whether you made money or lost money, the exit is where the outcome becomes final. A gain becomes real. A loss becomes permanent. And the identity you built around that position , “I am the person who spotted this stock early” has to be revisited.

That is why people avoid it. Not because they are careless. Because the exit forces an emotional event that the entry never does. Entry is a bet on the future. Exit is a judgement on the past. The human mind will almost always prefer the first over the second.

What actually happens when selling has no framework

When an investor has no structured approach to selling, the exit does not disappear. It just gets handed over to emotion. And emotion, in markets, follows a very predictable set of patterns.

- The first pattern is holding losers far too long.

A stock falls 15 percent. The investor does not sell because the loss does not feel real yet , it is still on paper. It falls another 15 percent. Now selling would mean admitting the original decision was wrong. That admission is painful enough that the investor reframes the situation: “It will come back.” “The fundamentals haven’t changed.” “I’ll sell when it reaches my buy price.” The position quietly becomes a trap , not because the market is trapping the investor, but because the investor is trapping themselves inside the discomfort of realising a loss.

Terrance Odean, a behavioural finance researcher at UC Berkeley, studied this using real trading records of over 10,000 accounts. His findings were sharp: investors were 50 percent more likely to sell a stock that had gone up than a stock that had gone down. They did not sell based on analysis of the business. They sold based on whether the position made them feel like they had succeeded or failed. The winners got sold. The losers got kept.

And the part that makes it expensive: the winners that were sold went on to outperform the losers that were kept by 3 % points over the following year. The investor did not just make a psychologically driven decision. They made one that directly cost them money ,by exiting the right position and staying in the wrong one.

- The second pattern is selling winners too early.

This one is quieter and often looks like discipline. A stock rises 25 percent. The investor sells because the gain feels fragile , it could disappear. The relief of booking profit is immediate. The regret of watching the stock double over the next two years is slow and difficult to measure.

This is loss aversion working in reverse. Daniel Kahneman and Amos Tversky showed decades ago that people feel the pain of a loss roughly twice as intensely as the pleasure of an equivalent gain. When you are sitting on a profit, the fear of losing that profit becomes louder than the logic of staying invested. The gain is already there. The mind says: protect it. And so the investor exits, not because the business stopped performing, but because the emotional cost of watching the number fluctuate became unbearable.

- The third pattern is the deadline exit.

This shows up especially among salaried investors. A goal is approaching , a down payment, a child’s admission, a family event. The investor needs the money, and the timing has nothing to do with what the stock or the market is doing. They exit because they have to, not because they should. And very often, this forced exit lands in the middle of a correction, because corrections do not check your calendar before arriving.

The problem here is not the goal. The problem is that the investor never planned the exit relative to the goal. They entered with a purpose but never built a timeline for getting out , one that accounts for market conditions, for the possibility of bad timing, and for the emotional pressure of needing money while watching a drawdown.

The cost of poor exits is not a theory

Morningstar publishes a study called “Mind the Gap,” which measures the difference between what a fund returned and what the average investor in that fund actually earned. The most recent edition, covering ten years of data ending December 2024, showed a gap of 1.1 percentage points per year. Fund returns averaged 7.3 percent annually. The average investor earned 6.2 percent.

Over ten years, that annual gap compounds into a meaningful difference in wealth. Not because the investor chose poorly. Because they left poorly.

In India, the pattern is visible in mutual fund data. AMFI reported that in FY24, gross inflows into equity schemes rose 28 percent. In the same period, SIP redemptions jumped 54 percent. Investors were entering and exiting at the same time but the exits were reactive. They were responses to short-term drawdowns, not to any structural change in what the fund was doing. The SIP was designed to remove emotion from investing. But the exit which was never designed reintroduced it.

Why nobody teaches selling

There is a structural reason for this imbalance.

The financial ecosystem — brokerages, content creators, advisors, influencers makes money from activity. A new buy generates a transaction. A new idea generates engagement. A recommendation generates clicks, followers, and revenue. The sell decision generates none of that. Nobody builds a following by saying “sit still” or “this is where you leave.”

Selling is also harder to package. A buy thesis fits neatly into a story: “This company is growing, this sector is expanding, this stock is undervalued.” A sell thesis requires nuance: “The growth has slowed relative to what the price assumed, the margin of safety has narrowed, and the capital has a better use elsewhere.” That does not fit in a reel. It does not generate excitement. It does not get shared.

So the education stays lopsided. The investor walks in knowing how to enter, and exits get treated as something that will work out naturally. They rarely do.

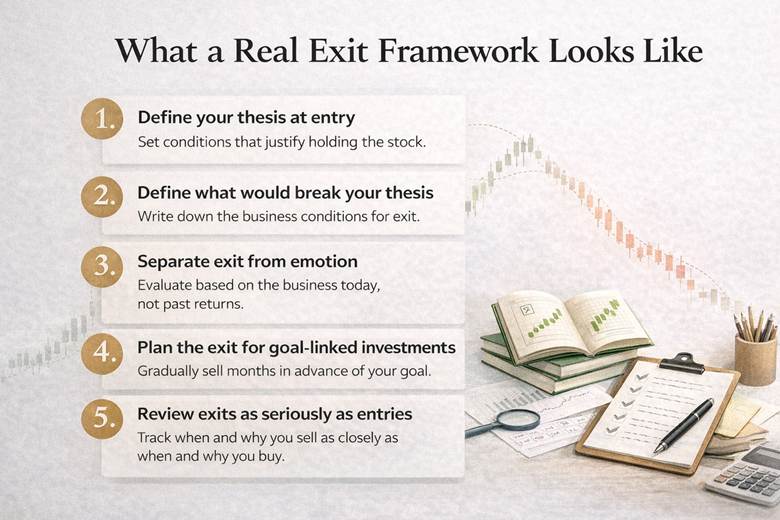

What a real exit framework looks like

The fix is not complicated. But it does require something most investors have never been asked to do: build a selling philosophy before you need to sell.

First, define the thesis clearly at the time of buying. Not “this stock looks good” , but what specifically has to remain true for you to hold this position? Revenue growing above a certain rate. Margins stable. Market position intact. Cash flow improving. If you cannot name the conditions that justify holding, you will never know when they have broken.

Second, define what would make the thesis wrong. Before a single rupee is deployed, write down the conditions under which you would exit. Not a price level. A business condition. Revenue declines for two consecutive quarters. The company takes on unexpected debt. A regulatory change damages the core model. Management makes capital allocation decisions you do not understand.

Third, separate the exit from the emotion of the position. This is the hardest part. The stock that has doubled still needs to be evaluated on what it is doing now, not on what it did for you. The stock that is down 40 percent also deserves the same honest evaluation. The exit should answer one question: based on where the business stands today, would you buy this stock at this price with fresh money? If the answer is no, the position deserves review regardless of whether it is sitting on a gain or a loss.

Fourth, plan the exit timeline for goal-linked investments. If money is meant for a specific purpose within three to five years, the exit should begin well before the deadline. Not all at once. Gradually. A phased exit over 12 to 18 months before the goal protects the investor from the risk of needing money during a drawdown. The worst version of selling is selling because you have no other option.

Fifth, review exits with the same seriousness as entries. Most investors track what they bought and why. Almost none track what they sold and why. Keeping an exit journal , even a simple one , forces the investor to confront their own patterns. Did you sell because something changed? Or because something felt uncomfortable? Over time, the answer reveals more about your investing behaviour than any portfolio tracker ever will.

Closing

Markets have made buying easy. Apps open in seconds. Screeners run on a tap. Content tells you what to enter and when. The entire infrastructure of modern retail investing has been built to reduce the friction of getting in.

Nobody has built the equivalent for getting out.

Entry is where confidence lives. Exit is where outcomes are decided.

Most investors spend years perfecting how they walk into a position. They never once practise how they leave.

That is the exit illusion. You think the hard part is finding the right stock. The hard part was always knowing when to let it go.