The ongoing Iran-U.S.-Israel war has tested Indian investors again. The market is reacting to real risk. The bigger question is whether investors are reacting to risk, or to panic.

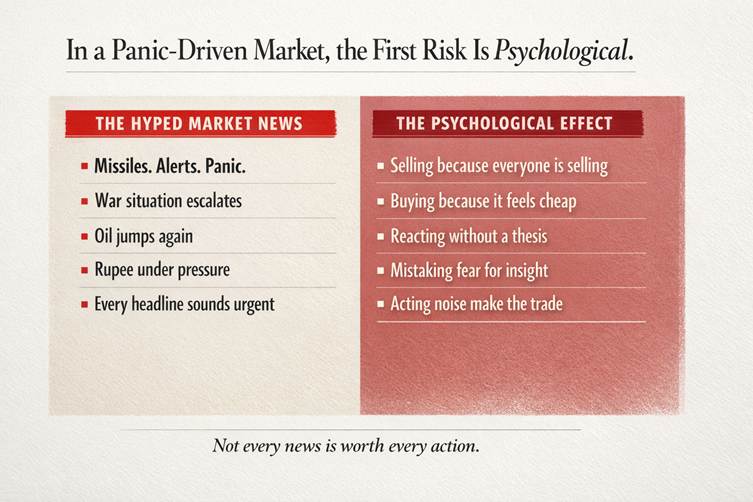

The headlines make it look simple. War escalates. Oil jumps. Markets fall. Experts shout. Screens flash red. Investors panic.

But markets are rarely damaged by the event alone. They are damaged by what the event does to the mind.

That is the part many people miss in times like this. The current conflict involving the U.S., Israel, and Iran is serious. It has already disrupted energy flows, pushed oil sharply higher, and increased pressure on economies that depend heavily on imported energy. India has felt that almost immediately through the rupee, foreign flows, bond yields, and market volatility. Reuters reported that the rupee fell to a record low this week as oil surged and foreign investors pulled back, while concerns rose around inflation, fiscal pressure, and the current account.

But if you have seen enough market cycles, you learn something important. In moments like these, investors do not get tested only once by the market.

They get tested twice.

First by the event. Then by their own reaction to it.

And very often, the second test does more damage than the first.

The risk this time is real. The Nifty 50 fell 8.1% in the first half of March, its worst fortnight since the COVID crash. Financials fell 9.8%. Banks fell 11.2%. Foreign portfolio investors sold ₹527.04 billion worth of Indian equities in that stretch. This is not a situation where the market is inventing danger for entertainment.

But there is still an important distinction to make. The market is trying to price changing probabilities. The investor is often reacting to emotional intensity. And that gap is where many bad decisions begin.

The market is repricing risk. The investor is absorbing pressure.

When geopolitical stress rises, the market does not move because it has reached certainty. It moves because the range of possible outcomes changes quickly.

Will crude stay high? Will the Strait of Hormuz become a deeper supply problem? Will inflation stay sticky? Will foreign investors continue to pull out? Will earnings estimates need to come down? Reuters reported that Citi and Nomura both cut their year-end Nifty targets because of those exact risks. Citi cut its target to 27,000 from 28,500. Nomura cut its target to 24,900 from 29,300. Citi also warned that prolonged disruption could shave 20 to 30 basis points off India’s FY27 growth and push inflation up by as much as 75 basis points.

That is the market’s job.

The investor’s experience is different. The investor is not sitting inside a probability model. The investor is sitting inside a noise machine — one that runs on alerts, TV panels, WhatsApp forwards, social media clips, and brokerage reactions, where every hour arrives dressed like history is breaking apart in real time.

That is what makes these phases dangerous. People do not react only to facts. They react to the emotional temperature around the facts. By the time they make a decision, they are often responding less to the market and more to the pressure of living inside nonstop commentary.

That is why panic does not only hit prices. It hits judgment.

Take February 24, 2022.

When Russia invaded Ukraine, the Nifty 50 fell 4.78% in a single session to 16,247.95. Reuters called it the index’s worst session since May 2020. Oil crossed $100 a barrel. The rupee suffered its worst day since April 2021. The mood that day was exactly what you would expect in a real shock: fear, certainty, and overreaction sitting together at the same table.

Then look at what happened next.

By March 30, 2022, Reuters reported that the Nifty had climbed to 17,449.75, a near seven-week high, as markets responded to signs of progress in peace talks and risk appetite improved globally. In other words, within a little over a month, the market had moved back above the invasion-day close.

What this tells us is simple. The first reaction can be brutal without becoming permanent. The investor who sold because the event felt too large did not protect capital. In many cases, that investor simply converted temporary fear into a permanent mistake.

Pattern two: Israel-Hamas begins, and the market reacts in stages, not in one straight line

Now take October 2023.

On October 9, 2023, the first Indian trading session after the Israel-Hamas war began, the Nifty 50 fell 0.72% to 19,512.35 as rising oil prices and inflation fears hit sentiment. The fall was real, and so was the concern that a wider Middle East conflict could hurt a large crude importer like India.

But the market did not keep moving in one straight line. By December 1, 2023, Reuters reported that the Nifty had hit a fresh record high, and by December 4, it closed at 20,686.80, well above the level at which the first shock had hit in October.

What this tells us is important. Geopolitical shocks do not always create a clean, linear market move. The market reacts to the first fear, then keeps reassessing as oil, yields, global risk appetite, and the probability of wider spillover change. Investors who treat the first fall as the full story often end up reacting to panic, while the market itself is still busy repricing probabilities.

Pattern three: The current U.S.-Israel-Iran shock is still unfolding, but the pattern is familiar

Now come to the present.

On March 2, 2026, the Nifty 50 fell 1.24% to 24,865.70 as crude jumped and the market began pricing a deeper Middle East risk. By March 30, the Nifty had fallen 11.31% through the month, closing at 22,331.40 — its biggest monthly decline since March 2020. But even within this fall, the market has not moved in one straight line. On March 10, it rebounded 0.97% as immediate fears cooled, before selling resumed and widened the losses further through the final week of the month.

What this tells us is important. The current correction is still live, so it would be careless to say stability is already back. But if you place it next to the earlier patterns, the rhythm looks familiar: a sharp fall, a partial recovery, fresh pressure, and then attempts to stabilize as the market keeps reassessing oil, inflation, currency risk, and foreign flows. That is why this phase should be seen as a process, not a verdict. In shocks like these, stability usually returns before confidence does. The real question is whether the investor can wait for that process to play out instead of reacting to every wave of fear.

For Indian investors, the real job is to track transmission, not theatre

Whenever conflict escalates, many people get trapped in the theatre of it. Maps. Missiles. Statements. Emergency meetings. Red tickers. Loud anchors. None of that helps you if your goal is to invest well.

For Indian investors, the real question is far more practical.

How does this travel into my market?

The answer is not complicated. Through crude. Through the rupee. Through imported inflation. Through FPI flows. Through sector-specific earnings pressure. Reuters noted that analysts were especially cautious on areas such as fertilizers, petrochemicals, and autos because of input dependence and macro sensitivity, while financials took the biggest hit because they remain the most foreign-owned major sector in the market.

That is why the right approach in times like this is not to track the loudest headline. It is to track the transmission.

If crude stays high for longer, that matters.

If the rupee remains weak, that matters.

If foreign selling stays broad and persistent, that matters.

If earnings assumptions need to be reset sector by sector, that matters.

Everything else is noise unless it starts affecting those variables.

The real investor mistake begins when trust shifts from business to mood

This is where the market correction becomes personal.

A stock falls sharply, and instead of asking whether the business has changed, people ask whether the situation feels scary enough to exit. A sector gets hit, and instead of reviewing balance sheet quality, pricing power, or earnings resilience, they react to the temperature of the moment.

That is usually where damage is done.

Trust has to begin with the business. Then you examine the market’s reaction.

Not the other way around.

If a company still has earnings power, a sound balance sheet, durable demand, and a competitive position that has not materially changed, then a panic-driven fall in the stock price does not automatically mean the investment case is broken. It may only mean the market is repricing macro risk for a period.

At the same time, discipline does not mean blind holding either. Some businesses are genuinely more exposed to oil, weak currency, imported inputs, or external capital. Those deserve review. That is the point. Good investing during a shock is not passive. It is selective.

If you are a serious long-term investor, do these five things before you act

First, check whether the business has changed, not only the stock price. Price can react faster than value. Business deterioration and market fear are not the same thing.

Second, separate a fear spike from a lasting macro shock. The current situation deserves respect because the transmission into India is real. But not every sharp fall deserves a full portfolio rewrite.

Third, do not let one week of panic rewrite a five-year plan. Ukraine in 2022 is a useful reminder here. The first move was severe. The lasting move was very different.

Fourth, reduce screen noise before you reduce portfolio exposure. Too much commentary damages judgment. During stressful periods, overconsumption of market noise is often more dangerous than volatility itself.

Fifth, act on evidence, not on emotional exhaustion. If fundamentals are changing, review the portfolio seriously. But if what has changed most is the emotional temperature around the market, patience is often the more intelligent decision.

Testing times reveal more than portfolio strength

Anyone can sound rational when markets are rising.

The real test comes when prices are unstable, headlines are aggressive, and uncertainty becomes expensive.

That is when you find out whether you built a portfolio or only built a story around a portfolio.

The current conflict has clearly created real market stress. That should not be dismissed. But another truth matters just as much: in moments like these, many investors lose more from misreading the situation than from the situation itself.

That is why the real discipline in markets is neither blind optimism nor blind fear.

It is the ability to ask, calmly and clearly:

Has the business changed? Or has the mood changed? Because markets do recover from shocks. What takes longer to recover is the damage caused by decisions made in panic.