When investors stop analyzing a company and start defending a belief, risk changes shape.

Some companies do not enter the market as stocks. They enter as movements.

That is what makes the SpaceX IPO conversation so useful for retail investors. It is not only a story about rockets, satellites, Starlink, artificial intelligence, Mars, or Elon Musk. Those are the visible parts. The more important part sits inside the investor’s mind: what happens when a company becomes so admired that questioning the price starts feeling like questioning the future itself?

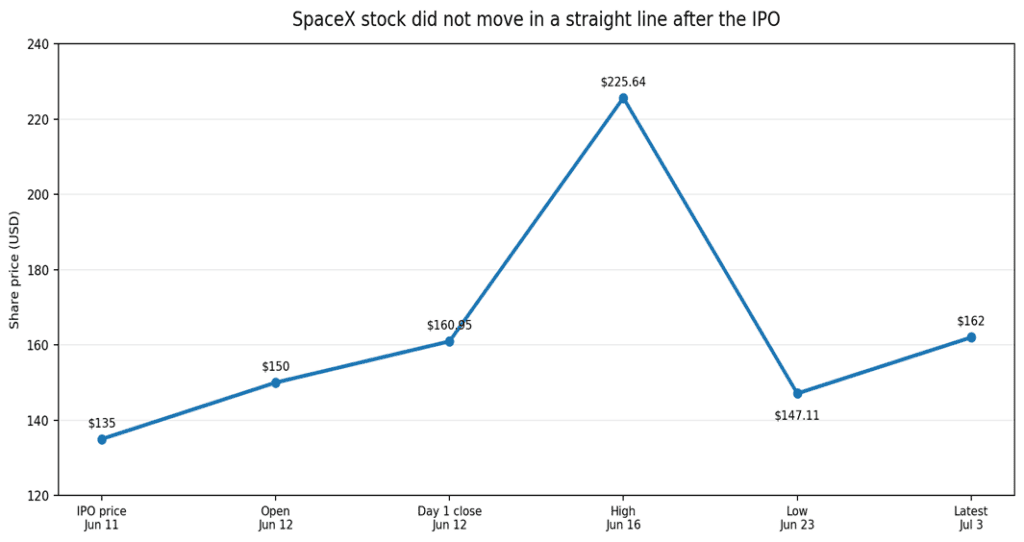

SpaceX is not an ordinary business story. Reuters reported that the company set its IPO price at $135 a share, raised $75 billion, and targeted a valuation around $1.75 trillion. Based on reported 2025 revenue of $18.67 billion, that placed the company at an unusually high trailing revenue multiple.

On debut, the stock opened at $150 and closed at $160.95, pushing its market value above $2 trillion. Within days, the stock had traded far higher, later corrected sharply, and was recently quoted around $162. It is still above the IPO price, but far below the peak that followed the first burst of public-market excitement.

This is the kind of price path that creates emotion before it creates analysis. The first buyer feels validated. The late buyer feels pressure. The person watching from the outside feels regret. The person who bought near the high starts searching for reasons to believe harder. In a normal stock, these are market movements.

In a fandom stock, they become emotional signals.

The company itself is real. The execution is real. Starlink reportedly crossed 10 million active customers across 160 markets by February 2026. SpaceX has built one of the most important industrial platforms of this generation. It has changed the economics of launches, turned satellite internet into a global consumer product, created a company that sits across aerospace, communication infrastructure, defence, and now the broader AI imagination.

That is not the debate.

The debate is whether retail investors can separate business admiration from investment discipline. This separation becomes difficult when the story is this powerful. A normal company asks investors to study revenue, margins, contracts, capital expenditure, competition, and regulation. SpaceX asks the investor to imagine a future where reusable rockets, satellite internet, orbital infrastructure, defence work, AI-linked data centres, and Mars sit inside one narrative.

At that point, the mind stops valuing one business. It starts valuing an entire possible future.

That is where fandom investing begins. Not when an investor likes a company. Liking a company is normal. The danger begins when the investor’s emotional attachment becomes stronger than his willingness to question assumptions.

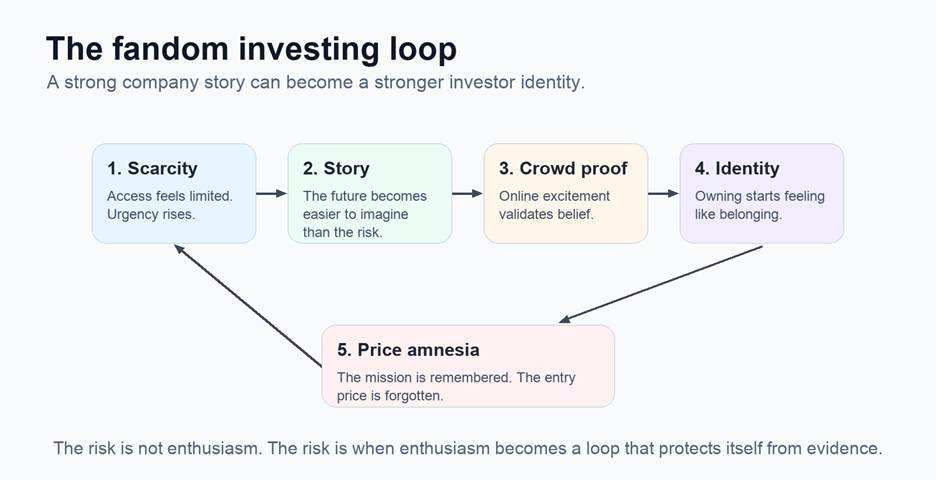

Visual pause: the stock moved from access, to validation, to volatility. That is exactly where investor emotion becomes unstable.

The first force is scarcity.

For years, most retail investors could not buy SpaceX directly. They could watch launches, read about private valuations, follow Starlink numbers, and see institutional investors build positions, but they could not participate easily. That absence matters. Scarcity does something unusual to the mind. It makes access feel like opportunity even before valuation is studied.

When the door finally opens, investors do not feel like they are simply buying a stock. They feel like they are being allowed into a room from which they were previously excluded. The decision becomes less about price and more about entry. This is why scarcity is dangerous. It changes the comparison. The investor is no longer asking whether $135, $160, or $200 is a fair price. He is asking whether he will regret not entering at all.

Regret is one of the strongest forces in investing. It can make patience feel like cowardice. It can make a high valuation feel acceptable. It can make a rushed entry feel like decisive action. The investor tells himself he is being bold. Very often, he is only trying to escape the pain of being left outside.

The second force is the memory of Tesla.

Many retail investors do not look at SpaceX only through SpaceX. They look at it through the emotional memory of Tesla. They remember the people who laughed at Tesla and were proven wrong. They remember the early investors who looked irrational for years and then looked visionary later. They remember the stock they did not buy, the gains they missed, and the lesson they think the market taught them: never bet against Elon Musk.

But that lesson is incomplete. Tesla’s past does not automatically make every future price reasonable. It proves that great businesses can surprise consensus. It does not prove that valuation stops mattering. This is where retail investors often make a silent mistake. They convert one extraordinary outcome into a rule of investing.

The mind likes simple stories. It likes to say, ‘People doubted Tesla and were wrong; people doubt SpaceX, so they may be wrong again.’ That sounds logical, but it skips the most important part: price. A company can be right about the future and still be a poor investment from the wrong entry point. The memory of a missed winner can be useful if it teaches humility. It becomes dangerous when it teaches surrender.

The third force is founder premium.

Elon Musk is not treated like a normal CEO by the market. He carries a founder premium that is partly financial and partly emotional. Investors do not only price current execution. They price the belief that he can enter impossible markets, absorb years of doubt, and eventually force reality to adjust around the company. That reputation has value. It would be naive to ignore it.

But founder premium has a limit. The harder question for investors is not whether Musk deserves a premium. The harder question is how much of that premium has already been paid upfront. At a certain valuation, the market is no longer rewarding execution after it happens. It is paying today for execution that may take many years to prove. That is where the risk changes.

There is a difference between respecting a founder and outsourcing your judgement to him. The first is rational. The second is fandom. In founder-led companies, retail investors often confuse personal admiration with business analysis. They begin to believe the founder can solve every problem: competition, regulation, capital intensity, execution delays, margins, and cyclicality. That is rarely how markets work. Even extraordinary founders operate inside ordinary constraints. Cash still matters. Time still matters. Competition still matters. Price still matters.

The fourth force is social proof.

IPO hype no longer travels slowly. It does not wait for annual reports, broker notes, or financial newspapers. It travels through clips, screenshots, posts, group chats, memes, newsletters, and influencers who compress a complex company into one emotional sentence. A story that should take hours to study becomes a caption that takes seven seconds to believe.

This matters because fandom investing is rarely an individual act. It grows within crowds, where shared excitement begins to look like proof. As the price rises, the story gains credibility, attracting more buyers and creating a false sense of safety. What feels like conviction is often just a feedback loop: enthusiasm drives the price, and the price reinforces the enthusiasm.

Social proof is especially powerful in stocks with a heroic story. Nobody wants to be the boring person asking about margins when the crowd is talking about Mars, AI, and the future of connectivity. But that boring question is usually where discipline lives. In a hype cycle, the investor who asks for numbers feels negative. In reality, he may be the only one still acting like an investor.

Put these four forces together, and the fandom loop becomes visible. Scarcity creates urgency. The Tesla memory supplies emotional proof. Founder premium reduces doubt. Social proof makes the crowd feel like confirmation. Once these forces combine, the investor stops asking, ‘What is this worth?’ and starts asking, ‘What if I miss it?’

That one question changes everything.

A disciplined investor can admire SpaceX and still question the valuation. A fan struggles to do both. For the fan, every risk sounds like negativity. Every correction sounds like manipulation. Every seller looks impatient.

Every short seller looks like an enemy. The stock is no longer an asset. It becomes a side.

This is why fandom investing is more dangerous than ordinary speculation. In speculation, the investor knows he is taking a risk. In fandom investing, the investor believes he is taking a stand. That belief makes exit difficult.

If the stock falls 20 percent, the fan says the market does not understand the company. If it falls 40 percent, he says long-term investors need patience. If it falls 60 percent, he searches for more people who still believe. The deeper the loss, the more emotionally expensive it becomes to admit that the entry price may have been wrong.

The irony is that none of this requires SpaceX to be a bad company. In fact, the opposite is true. Fandom investing is most dangerous when the company is genuinely impressive. Weak companies invite suspicion.

Great companies invite surrender. That is the lesson retail investors need from the SpaceX IPO hype. The question is not whether SpaceX is important. It is. The question is whether importance automatically justifies any price. It does not. A great company can change the world and still deliver poor returns if investors pay too much for the privilege of owning it.

This is where mature investing begins. Not by rejecting powerful stories, but by refusing to let powerful stories replace process.

Before buying into any company that has become a movement, the investor needs to slow down and ask four uncomfortable questions.

- What part of the valuation is supported by current business performance?

- What part depends on future markets that do not yet exist at scale?

- What am I assuming because I have studied the business?

- And what am I assuming because I do not want to miss the next Tesla?

Those questions protect the investor from confusing conviction with belonging. SpaceX may become one of the most consequential public companies of this era. It may also become one of

the clearest examples of how admiration can distort judgement when retail investors arrive after years of myth- building.

The real test will not be whether investors believe in SpaceX. Many already do. The real test will be whether they can still think like investors after they start feeling like fans.