Emerging markets look stronger when foreign money enters. But when that money leaves, investors learn which part of the rally was rented.

October 2024. FIIs sold ₹1,14,445 crore from Indian equities in a single month. All-time record. Bigger than the COVID crash selling of ₹65,816 crore in March 2020.

Your phone buzzed. Headlines screamed. Portfolio turned red. And the question that ran through every retail investor’s mind was the same: is something wrong with India?

That question was the mistake.

FIIs didn’t leave because India broke. They left because China’s Hang Seng was trading at 12x P/E while Nifty sat at 23x P/E. A 50% valuation gap. China also announced a stimulus package worth roughly Rs 116 lakh crore. Global funds did simple math: sell expensive, buy cheap. India happened to be expensive. China happened to get cheaper.

India’s Q2 FY25 GDP growth was still 5.4%. No structural break happened. The only thing that changed was relative attractiveness.

This is where the mistake begins. Foreign capital is often treated like belief. Most of the time, it is only allocation.

India may still be strong. The companies may still be good. The long-term story may still be intact. But if another market becomes cheaper, US yields become more attractive, the dollar strengthens, crude oil rises, or global risk appetite changes, foreign money can move.

That does not always mean the country has failed. It means the capital had no loyalty clause.

FIIs Are Not Owners. They Are Tenants.

A global fund manager is rarely asking: “Do I love this country?” They are asking: “Where does this money earn the best return for the risk I am taking right now?”

That question can change very quickly.

India may still be strong. The companies may still be good. The long-term story may still be intact. But if another market becomes cheaper, US yields become more attractive, or global risk appetite changes, foreign money moves.

That does not mean the country has failed. It means the capital had no loyalty clause.

A factory cannot leave overnight. A supply chain cannot be sold by clicking a button. Long-term business investment has friction. It is built into the country.

Portfolio money is different. It can enter quickly, support prices, and leave quickly when risk-reward changes.

That is why emerging markets often look stronger when foreign capital enters. The market receives liquidity, the currency feels supported, valuations expand, and everyone feels comfortable.

But comfort is not the same as resilience. If the comfort depends too much on capital that can leave overnight, part of the market’s balance sheet is rented. And when rented money leaves, retail investors feel the shock first.

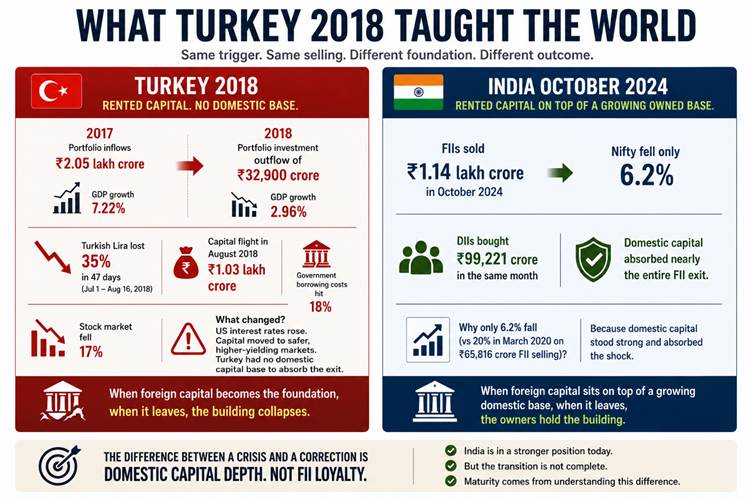

What Turkey 2018 Taught the World

In 2017, Turkey received portfolio inflows worth roughly Rs 1.6 lakh crore. GDP grew 7.22%. Foreign capital loved Turkey.

In 2018, same country, same government: portfolio investment swung to an outflow of roughly Rs 27,000 crore.

In just 47 days between July 1 and August 16, 2018, the Turkish lira, Turkey’s currency, lost 35%. Capital flight in August 2018 alone was roughly Rs 1 lakh crore. Government borrowing costs hit 18%. Stock market fell 17%.

What changed? The US Federal Reserve raised interest rates. Capital found a safer, higher-yielding home. Turkey had no domestic capital base to absorb the exit. The country did not only face market volatility. It faced a wider confidence crisis.

That is what happens when foreign capital becomes the foundation rather than a supplement.

India is in a stronger position today because the domestic investor base has deepened. SIP flows have become more consistent. Mutual funds are larger. Retail participation has grown. DIIs can now absorb shocks that would have been far more dangerous in earlier cycles.

But this should not make investors careless. It should make them more mature.

India is slowly moving from a market that needed foreign approval to a market that can increasingly stand on domestic ownership.

That transition is important. But it is still a transition.

October 2024: Same Selling, Different Result

FIIs sold ₹1.14 lakh crore in October 2024. But Nifty fell only 6.2%.

Why only 6.2% on double the selling of March 2020 when markets fell 20%?

Because DIIs bought ₹99,221 crore in the same month. Domestic capital absorbed nearly the entire FII exit.

Turkey had rented capital with no domestic base. When tenants left, the building collapsed. India in 2024 had rented capital sitting on top of a growing owned base. When tenants left, the owners held the building.

The difference between a crisis and a correction is domestic capital depth. Not FII loyalty.

Why Retail Investors Misread FII Selling

A retail investor may be thinking in years. A global fund may be thinking in quarters or risk limits. A retail investor may believe India is a better long-term story than China. A fund manager may still move money to China for a few months because China has become cheaper.

Both can be logical. But they are playing different games.

This is why retail investors panic when FIIs sell. They think the foreign investor has changed their view on the country. Often, the foreign investor has only changed their allocation.

That one misunderstanding creates unnecessary fear.

3 Questions to Ask Before You React

Question 1: Is this India-specific or global reallocation?

India-specific: FIIs selling only India. Trigger is GDP slowdown, earnings miss, policy uncertainty. Real signal. Investigate.

Global reallocation: FIIs selling multiple markets simultaneously. Trigger is US rate changes or a large market getting cheaper. Not about India. Do not react as if it is.

In October 2024, eight out of eleven tracked Asian markets saw FII outflows simultaneously. Global reallocation. Not an India verdict. Correct response: hold or selectively add.

Question 2: What is the DII absorption gap?

FII selling alone tells you nothing. FII selling minus DII buying tells you everything.

October 2024: FIIs sold ₹1,14,445 crore. DIIs bought ₹99,221 crore. Gap: ₹15,224 crore. Small gap. Market fell 6.2%.

March 2020: FIIs sold ₹65,816 crore. DII buying significantly lower. Large gap. Market fell 20%.

Gap under 20% of FII selling: domestic market absorbing the shock. Don’t panic.

Gap above 50% of FII selling: no floor. Genuine warning.

Track the gap. Not just the FII number.

Question 3: Is FDI also weakening?

FPI is fast money. Monthly noise.

FDI is ownership money. It builds factories, hires workers, creates supply chains, and usually carries a longer-term commitment.

India’s FDI picture is more nuanced now. Gross FDI inflows rose to a record of roughly Rs 8.04 lakh crore in FY2026, compared with around Rs 6.85 lakh crore in the previous year. That tells us long-term foreign interest has not disappeared. But net FDI was only around Rs 65,000 crore because repatriation, disinvestment, and overseas investment by Indian companies absorbed a large part of the headline inflow.

When FPI falls but gross FDI remains healthy: temporary market noise. Do not panic only because portfolio money moved.

When FPI falls and net FDI also weakens sharply: structural concern. Investigate.

When FPI falls but long-term FDI keeps improving: the market may be misreading short-term fear as long-term weakness.

The Real Shift Happening in India

FII ownership: 14.7%, a 14-year low. DII ownership: 18.9%. For the first time domestic institutions hold a larger share than foreign portfolio investors.

SIP contributions in April 2026: ₹31,115 crore. The 62nd straight month of positive equity mutual fund inflows: ₹38,440 crore in April 2026.

India is slowly moving from a market that needed foreign approval to a market supported by domestic ownership.

That is the difference between a rented balance sheet and an owned one.

FIIs Are Tenants

They pay rent when the price is right. They leave when they find a better deal. Loyalty was never the contract.

Next time FIIs sell, you now have three questions instead of one panic reaction.

Is this India-specific or global reallocation?

What is the DII absorption gap?

Is FDI also weakening?

Answer those three. Then decide. When FIIs leave, the market may still shake. But it no longer has to collapse every time the tenant changes their mind.