200 Pages to 2 Minutes: How Compression Changes Investor Judgement

If you invest in stocks, you are already living through a change in how research gets consumed. Company annual reports run into hundreds of pages. Analyst reports land after every quarter. Earnings call transcripts add another layer. Most investors do not have the time or patience to absorb all of it.

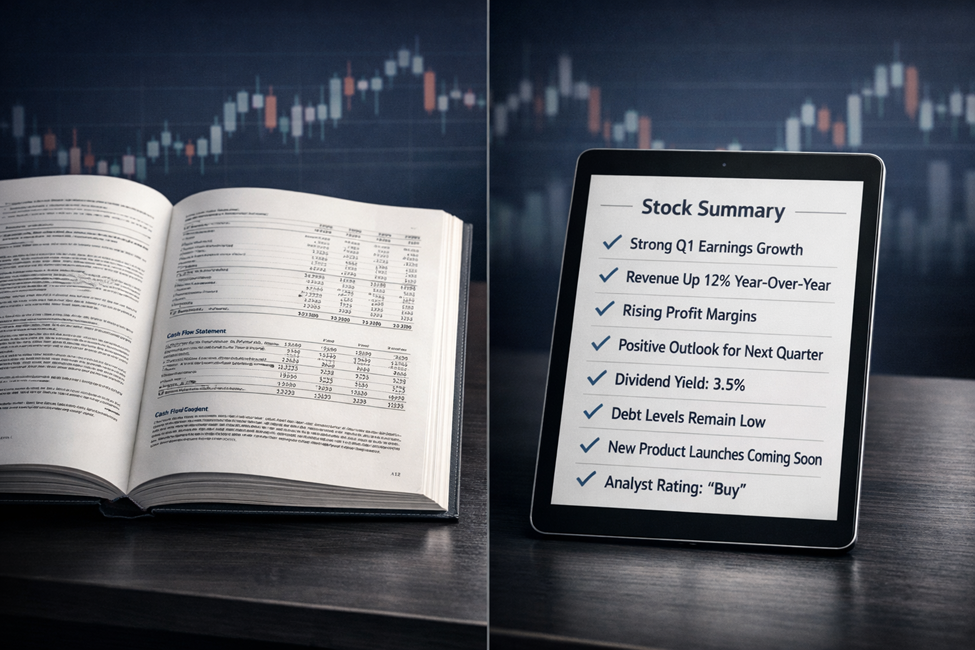

AI summaries solve that. You paste a document, you get the highlights, you move on. The convenience is real. The risk is real too, and it has nothing to do with AI being good or bad. It has to do with what happens inside your head when complex information gets compressed into ten bullet points.

A clean summary does something powerful. It makes you feel informed quickly. In stock markets, quick confidence is rarely free.

The danger is not that AI summaries are inaccurate. The danger is that they feel complete and completeness is what stops investors from asking the questions that matter most.

What Compression Removes from Stock Research

A company’s annual report and a well-written analyst report are long because businesses are layered. Most of the risk in a stock does not sit in the headline numbers. It sits in the conditions under which those numbers remain true.

A summary gives you the surface narrative. Revenue is growing. Margins are stable. Debt looks fine. Outlook seems steady. That can be accurate and still miss the part that decides outcomes.

The missing part is texture. Texture is where you see whether growth is cash-backed, whether working capital is stretching, whether debt is comfortable or merely parked for now, whether one segment is carrying the whole story, whether management language has become careful, whether the business is becoming sensitive to a single variable like rates, regulation, or one customer.

Compression does not remove risk. It removes contact with uncertainty. That is why it changes investor judgement.

The Psychology That Makes Summaries Dangerous

The human mind loves information that is easy to process. When something reads smoothly, it feels more true. When it feels more true, it feels safer to act on. Behavioural economists call this cognitive ease and markets have always been its hunting ground.

You read ten crisp bullets and your brain quietly concludes that you understand the stock. You feel like you have done the work. You feel ahead of the crowd, because you processed a large document in two minutes.

That feeling is the trap. Not because the summary is wrong, but because it creates a false completion signal. Research feels finished, even though the most important questions have not been touched.

Markets do not punish you for missing information. Markets punish you for acting like you have certainty.

Where Retail Investors Pay for This Mistake

Most investors worry about accuracy. They ask whether a summary missed a key point. The larger risk is what happens after reading it.

A clean summary produces quick conviction. Quick conviction inflates position size. Inflated position size makes small surprises expensive.

Portfolios rarely get damaged by one wrong idea. Portfolios get damaged when a lightly-checked idea is treated like a high-certainty bet. That is why this is not an AI article. This is an investing process article. AI can help you move faster. It cannot tell you how fragile the story is. That still requires judgement.

Use the Summary as an Index, Then Touch the Risk

A useful way to think about AI summaries in stock investing is this: let the summary tell you what the story is, then spend a few minutes checking what could break it.

Take any widely-followed stock — a Nifty 50 name. TCS, Reliance, HDFC Bank, ITC. Pick a company that feels familiar and well-covered. You run the annual report or analyst report through an AI tool. You get something like: Growth healthy. Margins stable. Balance sheet strong. Outlook steady.

Now you do a ten-minute check that forces you to touch the parts summaries usually compress too aggressively. Start with cash, then move to fragility, then run one scenario test.

1. Cash Flow in Three Minutes

Open the cash flow statement and compare net profit with operating cash flow. If profit and operating cash flow move together, the story is cleaner. If profit looks strong and operating cash flow is weak or inconsistent, slow down and look for the driver.

It is usually working capital movement or capex intensity. Receivables stretching is not a small detail. Inventory building is not a small detail. These are often the first places where the stock narrative starts to wobble and they are also exactly where several high-profile Indian corporate blowups have first shown their seams. IL&FS and DHFL both had years where profit looked stable while cash deteriorated. The receivables were the tell.

A summary will tell you revenue grew. Cash flow tells you whether the business collected what it sold.

2. Fragility Scan in Four Minutes

Open the notes and scan the usual hiding spots. You are not reading the whole report. You are looking for dependencies.

For an IT services company like TCS, scan receivables and contract language. Look for cues on pricing, collections, and any shift in revenue recognition wording.

For a bank like HDFC Bank, scan asset quality and provisioning language. Look for the tone around slippages and concentrations, and notice any subtle changes in risk classification language.

For an FMCG or manufacturing business like ITC, scan inventory commentary, raw material sensitivity, and contingent liabilities.

For a diversified company like Reliance, scan segment reporting, debt maturity profile, and capex commitments because a group story is often carried by one engine and weakened by another.

You are not searching for scandal. You are locating conditions.

3. One Scenario Test in Three Minutes

Write two lines. What has to go right for the story to hold? What breaks first if it does not?

This is the difference between reading and investing. Stock investing is scenario work. Summaries are built to summarise, not to pressure-test.

The Part Many People Ignore: Leverage Loves Compressed Confidence

This is where the modern market makes the overconfidence problem significantly worse and the article’s most important point is buried here.

Today, an investor can move from a summary to a trade in minutes, and that trade can easily involve leverage through options or margin. The summary does not just compress information. It compresses the time between forming a view and taking a position.

When conviction forms quickly, leverage becomes tempting. And leverage makes the market’s feedback brutal.

A small miss in cash flow. A small change in guidance tone. A small regulatory development. A mild disappointment in one segment. None of it needs to be catastrophic for a leveraged position to feel catastrophic.

Weekly options are the sharpest version of this problem. An investor reads a clean AI summary, feels conviction, buys short-dated options because the trade ‘feels obvious’ — and loses the entire premium on an earnings report that was merely fine rather than exceptional. This is not a rare event. It is a pattern.

Compression increases conviction speed. Conviction speed increases exposure. Exposure increases fragility. This chain is why a summary-led workflow needs a position sizing rule — not just caution, but a rule.

A Position Sizing Rule That Fits Real Life

You do not need a perfect system. You need a repeatable one.

If your understanding comes mainly from a summary, treat the stock as a candidate, not a conviction. Summary only should stay as watchlist or a tiny starter. Summary plus the ten-minute check earns a starter position. Scaling comes after deeper reading , when you can describe the downside in plain language and you know what would change your mind.

Scaling protects you from being too big too early. Being too big too early is how retail investors turn small errors into portfolio damage.

The Market Structure Angle: Identical Summaries Create Crowded Trades

There is a broader effect that is easy to underestimate. When many investors rely on similar compressed outputs from similar AI tools, interpretation starts to converge. The framing becomes uniform. The same bullet points become the same trade. The same trade becomes crowded.

Crowding in Indian equities is already driven heavily by index flows, institutional mandates, and momentum strategies. Retail convergence on a single AI-generated narrative adds a new layer to that. It is unlikely to move a Nifty 50 name dramatically on its own but in mid- and small-cap stocks, where liquidity is thinner and price impact is larger, homogeneous summaries leading to homogeneous positioning is a real risk.

Crowding stays invisible during good periods. It becomes obvious when one detail breaks the story and everyone reacts together. Independent judgement is not a philosophical idea. It is a practical defence against crowded narratives. Your ten-minute second step gives you that independence.

The Right Way to Think About AI in Stock Market Research

AI summaries belong in stock market workflows. They reduce the cost of scanning. They help investors organise information. They can save time without lowering quality when used correctly.

Correct use has one principle. AI speeds up your first layer. It does not replace your second layer.

The second layer is where investing lives. Cash flow reality. Balance sheet conditions. Segment truth. Risk language. Scenario thinking. Position sizing that matches the depth of work.

Ten bullet points can tell you the story. They cannot tell you how fragile the story is. That part still needs investor judgement and the market still charges full price when you skip it.

Use the summary to find the story. Use your own eyes to find the risk. That division of labour is what separates an investor from someone who is merely well-informed.