There has been a growing narrative over the past year suggesting that India is in the midst of a historic capex boom. From infrastructure and manufacturing to PLI-linked incentives and public sector investments, the theme of capital expenditure has dominated market conversations. But as always, the key question for investors remains: what does the data actually show?

This piece explores whether the capex cycle is as widespread as believed, or if we are still in the early stages of revival. The objective is to help investors distinguish between optimism and execution, and to position accordingly.

What the Data Tells Us

Let’s start with the numbers.

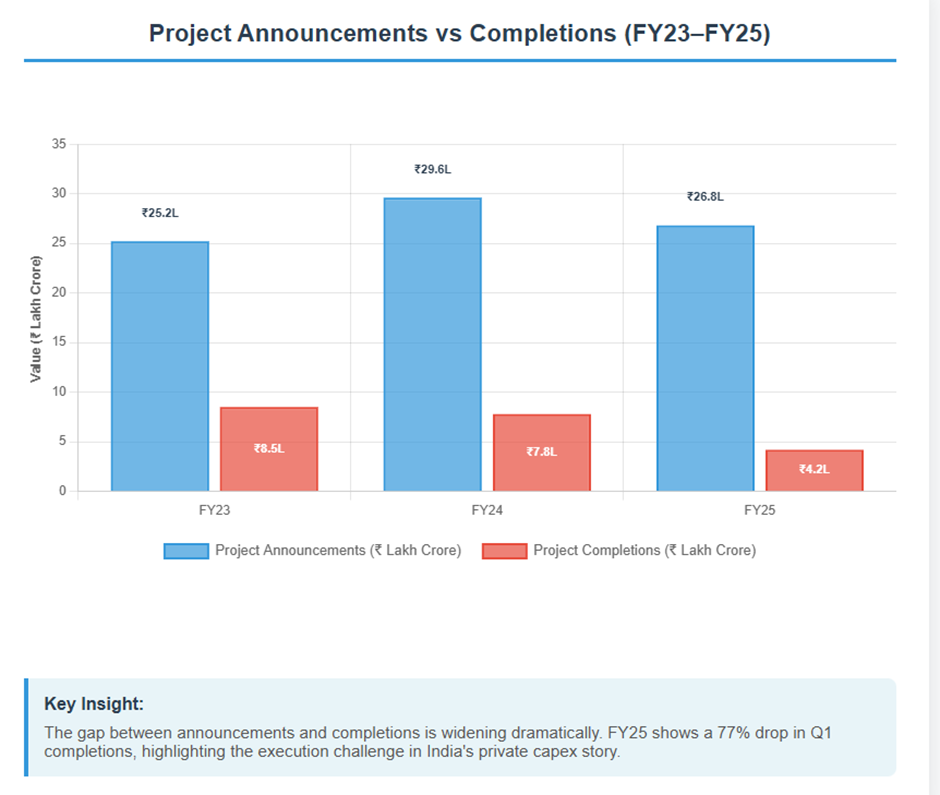

According to CMIE, the value of new private sector project announcements in FY25 stood at ₹26.8 lakh crore, a 9% decline from FY24, which recorded ₹29.4 lakh crore. In comparison, FY23 had ₹25.3 lakh crore worth of announcements. More telling is the state of execution: in Q1 FY25, project completions fell by 77% year-on-year, and the full fiscal saw each quarter post double-digit declines.

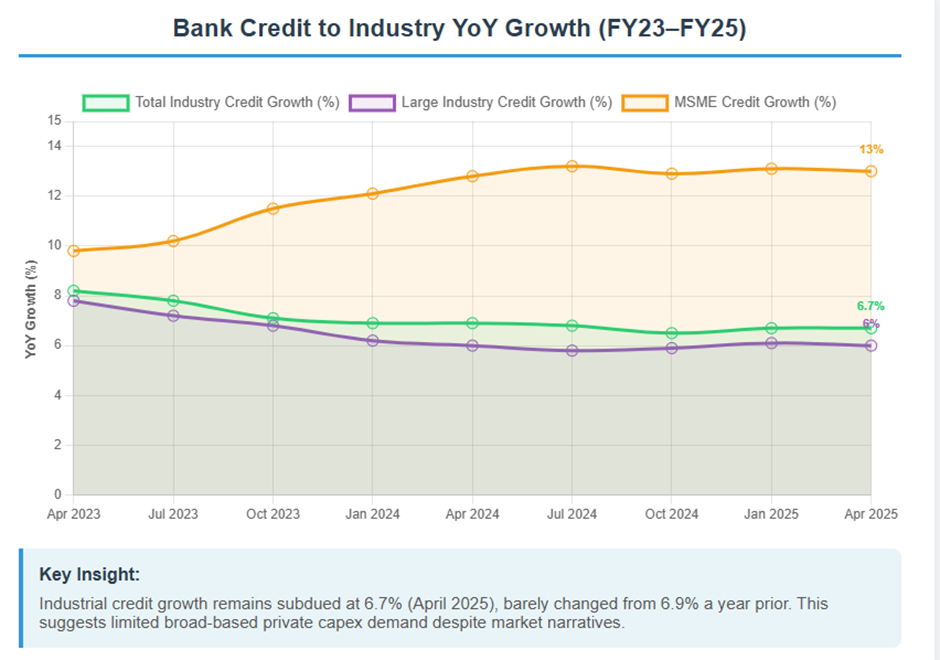

At the same time, bank credit growth to industry, a strong proxy for capex deployment, was 6.7% as of April 2025, largely unchanged from the 6.9% figure a year prior. Lending to large industries grew just ~6% YoY, with the stronger momentum observed in MSMEs (13% YoY growth), according to RBI data.

Where Activity Is Concentrated

Today’s capex momentum is concentrated in the public sector, especially in strategic infrastructure.

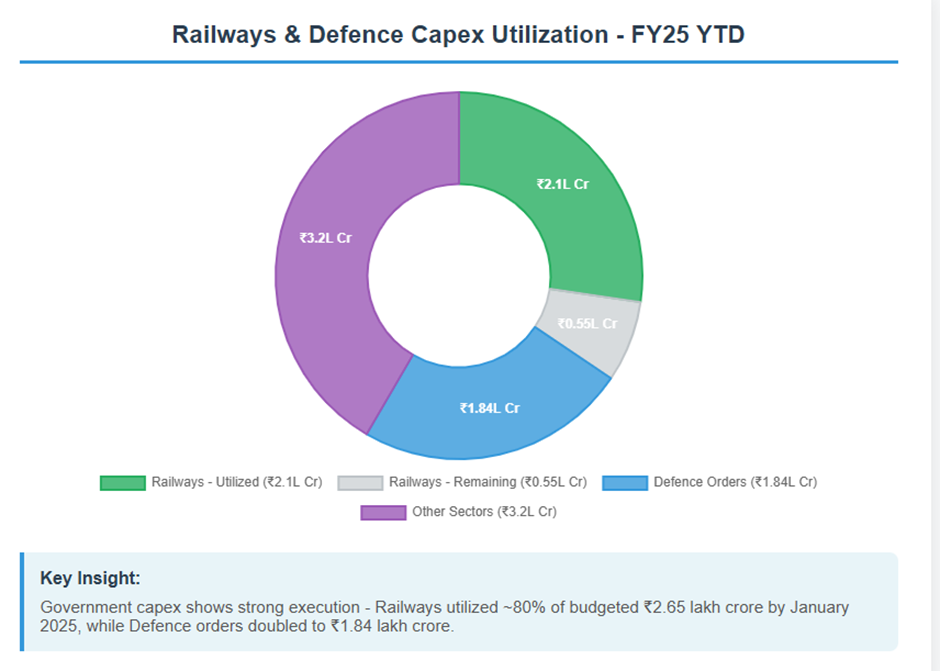

- Railways: Of the ₹2.65 lakh crore capital outlay for FY25, ₹2.1 lakh crore (~80%) was utilized by January, spent on track doubling, electrification, 1,300+ station upgrades, and Vande Bharat trains.

- Highways: MoRTH completed 12,300+ km of highways in FY24, targeting 13,000 km for FY25. NHAI recently awarded projects worth ₹2 lakh crore, nearing 80% execution under Bharatmala Phase-I.

- Defence: HAL’s order book nearly doubled to ₹1.84 lakh crore by March 2025, driven by Tejas jets, trainer aircraft, and helicopters. DRDO and private firms are scaling Make-I/II production and exports.

Capital Goods: Forward-Looking Clues

The capital goods ecosystem is heating up. Larsen & Toubro (L&T) reported a record order book of ₹5.8 lakh crore as of March 2025. Industry-wide, cap goods firms saw 24% YoY order inflow growth in FY24, and ~10% sequential growth in H1 FY25.

This suggests that companies supplying heavy machinery, electricals, and EPC services are already monetizing the early phase of the capex cycle.

The Private Sector: Turning Up, Cautiously

While public capex leads the way, private players are beginning to follow — slowly, but measurably. The headline projection of ₹11 lakh crore in corporate capex for FY25 is backed by rising capacity utilisation and cleaner balance sheets, but actual deployment remains uneven.

Who’s Spending?

| Category | Details |

| Key Investors | • Tata Group: ₹24,000 Cr in steel & EV plants (Tamil Nadu, Maharashtra) • Reliance: ₹75,000 Cr in green energy, digital infra, retail • Adani Group: ₹1.2 lakh Cr in ports, airports, defence (FY24–26) • JSW & Mahindra: ₹10,000+ Cr in steel & EV hubs |

| Execution Underway | ~35–40% of projected private capex is already in execution: • EV manufacturing (Tata, Ola, Mahindra) • Data centers (Jio, Nxtra) • Steel, cement, renewables (JSW, UltraTech, Waaree) |

| Key Bottlenecks | • Land and JV delays in semiconductors and solar • PLI disbursal and compliance friction • High borrowing costs through FY24 • Import competition in textiles and chemicals |

| Summary | Private capex is underway, but it’s selective and led by large corporates with strong balance sheets not yet a broad-based recovery. |

The private capex cycle has begun, but it’s sector-specific and balance-sheet-led, not yet a broad-based trend.

Positive Signals to Track

- Capacity utilisation in manufacturing stood at 74.7% in Q2 FY25, according to RBI’s OBICUS survey, comfortably above the long-term average of ~72%. This level has historically served as a trigger zone for fresh private investment, especially in capacity-driven sectors like cement, auto, and steel.

- Auto and EV manufacturing is gaining momentum. Tata Motors has commenced construction on a new EV-only facility in Tamil Nadu. Ola Electric is scaling its FutureFactory in Krishnagiri, and Mahindra has committed over ₹3,000 crore towards EV hubs in Pune and Zaheerabad. Combined, the top players have committed more than ₹10,000 crore for FY25–27, indicating confidence in the long-term domestic EV demand story.

- Defence manufacturing and industrial automation are seeing deployment beyond just MoUs. Bharat Forge, L&T Defence, and Adani Defence have announced production-linked expansions across artillery systems, drone components, and aerospace. With confirmed orders spanning 3–5 years, this vertical is transitioning from policy promise to the delivery phase.

- New-Age Infrastructure: The demand for data centers and digital infrastructure is exploding, leading to multi-billion-dollar investment commitments from both domestic and global players.

- Advanced Manufacturing: The PLI scheme is maturing. Beyond mobile assembly, we are seeing capex in higher-value segments like semiconductor components, speciality chemicals, and pharmaceutical APIs.

Investment Implications

For investors, the evolving capex data highlights three actionable insights:

- Separate narrative from execution. A stock being positioned as a ‘capex play’ doesn’t automatically mean it’s participating in the cycle. Look for signs of real monetisation — visible order wins, capex deployment updates, and revenue or margin traction. Deep dive into investor presentations and quarterly calls to validate the story.

- Back the ecosystem. Companies that support infrastructure, such as capital goods makers, EPC contractors, and infra financiers, are already seeing business momentum. These segments tend to benefit early and disproportionately in a capex cycle due to recurring demand visibility and project-linked revenue models.

- Track enabling indicators. Keep an eye on high-frequency data: monthly credit growth to industry, order booking trends, government capex disbursals, and sector-specific triggers (like EV policy clarity or defence export approvals). These will be the early signals of a wider private capex pickup.

In short, the capex story isn’t uniform, but that’s what makes it investable. The edge lies in being selective, data-driven, and early.

- Differentiate narrative from execution. Not every capex-themed stock is backed by deployment. Validate via actual order books, deliveries, and revenue conversion.

- Focus on ecosystem players. Capital goods, EPC firms, and infra financiers are already monetising the current phase.

- Monitor enablers. Credit growth, execution timelines, and public sector disbursals will determine when the broader private cycle accelerates.

Conclusion

India’s capex cycle is underway, but not uniformly. Public expenditure is doing the heavy lifting, while private capex especially outside select verticals remains conservative.

That said, rising utilisation, healthy corporate balance sheets, and robust order books suggest the groundwork is being laid. For investors, the key is to position early, but selectively with execution-backed exposure rather than sentiment-driven bets.

When in doubt, let the numbers lead.