The old investing promise was simple: invest the same amount, every month, and ignore the noise. The next one may be smarter: define the rules in advance, then let the system adjust when markets and life change.

SIPs solved a real problem

They made investing possible for people who would otherwise keep waiting

The SIP became popular because it fixed a very human problem. Most retail investors do not struggle with the idea of compounding. They struggle with action. They wait for a correction, then for a better correction, then for more clarity, and by the time clarity arrives, the market has moved and the habit never begins.

The SIP changed that. It turned investing into a standing instruction. It reduced hesitation. It reduced the urge to time every entry. AMFI still describes the SIP in exactly those simple terms: a fixed amount invested at fixed intervals, with instalments that can start as low as ₹500, and even ₹250 under Chhoti SIP. That simplicity is the reason the habit scaled and scale it has.

As of January 31, 2026, the Indian mutual fund industry’s AUM stood at ₹81.01 lakh crore, with 26.63 crore folios overall and about 20.43 crore folios in equity, hybrid, and solution-oriented schemes where retail participation is concentrated. Monthly SIP collections for January 2026 stood at ₹31,002 crore. This is no longer a niche savings habit. It is one of the core operating systems of retail investing in India.

The flaw is not systematic investing

The flaw is blind systematic investing

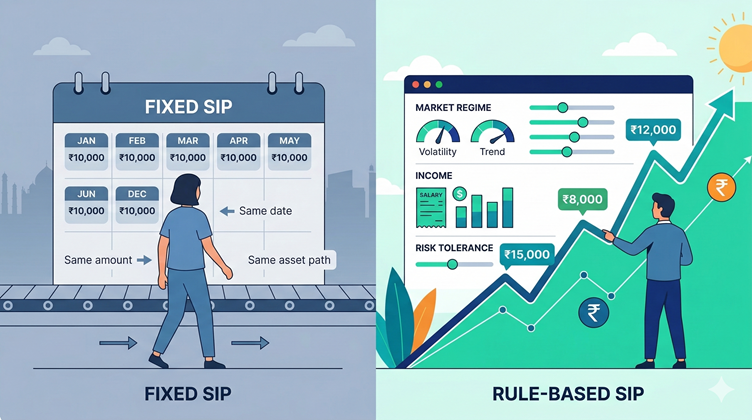

A classic SIP carries one hidden assumption: that every month deserves the same investing behaviour.

Same amount. Same date. Same asset path.

That was a good enough design when the main mission was to get investors started. It is a weaker design when the mission becomes staying invested through different market regimes and different life situations.

Because a calm market, a panic market, a year of strong income, and a year of financial strain are not the same environment. Yet the traditional SIP structure behaves as if they are. It treats discipline as repetition, even when repetition may ignore context.

That is the real criticism. Not that SIPs are wrong. Not that long-term investing is broken. The criticism is narrower, and more serious: a fixed instruction is helpful, but it is still a blunt instrument.

Markets change fast

Investor lives change faster

The easiest way to see the weakness of blind automation is to look at stress.

In its March 2020 Market Pulse, NSE noted that the Nifty 50 had fallen 6.4 percent in February and that selling intensified in March, with the Nifty VIX rising 448 percent year to date during that period. That was not ordinary volatility. That was a market shock.

Now place that next to real households.

A salaried employee with a stable income and a six-month emergency buffer is living in a very different financial reality from a business owner whose cash flows can disappear for a quarter. A 29-year-old building wealth for the next 25 years can tolerate drawdowns differently from a 57-year-old planning retirement. A household dealing with a medical emergency should not be forced into the same risk behaviour as a household with rising savings and low fixed obligations.

Yet the classic SIP engine treats them the same way. It acts like the investor is a bank mandate with a pulse.

That is where the next decade will likely force a change.

The next system will not guess the market

It will read context and act within rules

The future of investing is not a machine that magically predicts tops and bottoms. That story sells well and ages badly.

The more realistic future is a rule-based investing engine that reads context and makes limited adjustments inside pre-decided boundaries.

That means the investor still makes the important decisions in advance. The investor sets the broad asset allocation, defines the purpose of the portfolio, chooses risk limits, and decides what should happen when certain triggers are hit. The system then executes those rules without requiring a fresh emotional debate every month.

That is a meaningful shift. Today’s SIP says, “invest ₹10,000 every month.” A next-generation system could say, “invest ₹10,000 in normal conditions, but reduce to ₹7,000 if monthly free cash flow drops below a threshold; pause top-ups if the emergency fund falls below six months of expenses; increase contribution gradually after a deep drawdown only if income remains stable.”

That is still disciplined investing. In many ways, it is more disciplined. The rule survives. What disappears is the blind repetition.

What flexibility will actually look like

The change will be operational, not philosophical

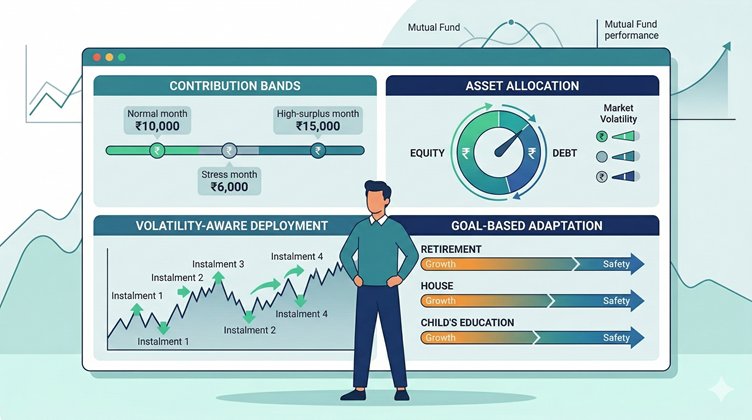

- The first big change will be contribution flexibility.

Instead of one fixed SIP amount forever, investors will likely use contribution bands. Normal month: ₹10,000. Stress month: ₹6,000. High-surplus month: ₹15,000, but only if liquidity goals are already funded. The system will stop treating every month as equally investable.

- The second change will be allocation flexibility.

Instead of sending every rupee into the same asset mix regardless of conditions, the system could shift fresh money within a pre-set range. In normal conditions, perhaps 70 percent equity and 30 percent debt. In extreme volatility, fresh contributions may temporarily move to 55 percent equity and 45 percent debt or cash equivalents. After a large correction, the system may restore equity allocation gradually. That is not market timing in the dramatic television sense. It is risk budgeting.

- The third change will be volatility-aware deployment.

In a calm market, one monthly debit may be fine. In a highly unstable market, the system could break that month’s contribution into smaller tranches over two or three weeks. The investor still invests. The system simply stops pretending that a shock regime and a normal regime deserve identical execution.

- The fourth change will be goal-based adaptation.

A retirement corpus, a house down payment due in four years, and a child’s education fund should not be pushed through the same pipe. The next generation of platforms will likely separate money by horizon and purpose, then change risk based on those timelines. Long-term money can stay more patient. Near-term goal money should become more conservative automatically as the deadline approaches.

AI will matter here

But not in the way fintech marketing usually claims

The role of AI in investing will be less glamorous and far more useful than “predict the next rally.” AI will matter because it can read several layers of context at once. It can track cash flow patterns, spending pressure, portfolio drift, volatility, drawdowns, liquidity buffers, and goal deadlines together. A human adviser can do some of this periodically. A system can do it continuously.

That makes AI useful as a context engine.

It also makes AI useful as a behavioural warning layer. A good system should be able to say: your emergency fund has fallen below the threshold you defined, so your fresh equity contribution is being reduced. Or: your current action conflicts with the 10-year horizon and maximum drawdown rule you set earlier. Or: you are trying to redeem a large part of the portfolio during a volatility spike; this falls outside your normal policy and triggers a cooling-off review.

That is a much better use of AI than pretending it can outsmart the market every Tuesday.

AI will also make personalisation easier. Two investors should not receive the same investing instructions if one has a stable monthly salary, low liabilities, and 12 months of liquidity while the other has uneven business income, school fees, and two months of cash cushion. The traditional SIP framework largely ignores that difference. AI-enabled investing systems will not have to.

Guardrails are the real heart of the next model

Without guardrails, flexibility becomes an excuse for panic

This part matters most. The future is not “more freedom to change your mind.” The future is better guardrails. Those guardrails can be simple and practical.

Never let SIP continuity push the emergency fund below six months of essential expenses. Never allow equity exposure to rise above a pre-set ceiling, even during euphoric phases.

Reduce fresh equity contributions when volatility crosses a defined threshold. Pause SIP top-ups when income falls more than a certain percentage.

Increase deployment after corrections only within capped limits, not with emotional all-in decisions.

Force a 48-hour cooling-off period before a major redemption from long-term funds. Review the strategy quarterly unless a clearly defined trigger is hit earlier.

Separate long-term wealth creation from near-term spending goals so that one bad year in markets does not damage both.

The industry has already admitted the need for flexibility

Current SIP structures are quietly moving in that direction

The clearest proof is that SIP Pause is already a recognised feature in scheme documents. AMFI-hosted documents from fund houses lay out terms under which investors can pause SIP instalments for a defined period, often after completing a minimum number of instalments, with automatic restart rules built in. That means the industry already accepts a simple reality: life does not move in a straight line, and fixed investing instructions sometimes need breathing room.

But SIP Pause is still a blunt tool. It is an emergency brake. The next step is more sophisticated. Instead of only “pause or continue,” the system should be able to “reduce, redirect, stagger, rebalance, or resume” based on the rules the investor has already approved.

That is the real bridge from first-generation automation to second-generation investing systems.

The next decade belongs to better-designed automation

Not to blind rigidity, and not to emotional tinkering

India has already built the investing habit. The numbers prove that. Monthly SIP contributions of ₹31,002 crore and an industry AUM of ₹81.01 lakh crore show that the retail investing engine is alive and expanding.

So the next question is not whether people should invest systematically. They should. The next question is whether the system itself can become more intelligent.

I think it will.

Not by replacing discipline with prediction. Not by encouraging investors to react to every headline. Not by handing over all judgment to a black box.

It will improve by doing something simpler and more useful.

Set the rules carefully. Define the guardrails in calm periods. Let the system adjust when markets or life move outside the normal range. Protect liquidity before forcing risk. Preserve discipline without worshipping rigidity.

That is where investing systems are headed. And frankly, that is where they should be headed.