After decades in these markets, I’ve seen plenty of schemes. But what Jane Street allegedly pulled off in India? This is systematic theft dressed up as smart trading.

Let me tell you what really happened here. Jane Street, one of Wall Street’s biggest algorithmic trading firms, allegedly ran a $4.3 billion operation that picked the pockets of millions of Indian retail traders.

I’ve been in these markets for years, and I know market manipulation when I see it. What India’s regulator SEBI uncovered isn’t just aggressive trading, t’s a blueprint for how modern technology can systematically steal from ordinary investors.

What Actually Happened? A $4.3 Billion Playbook with a Behavioural Twist

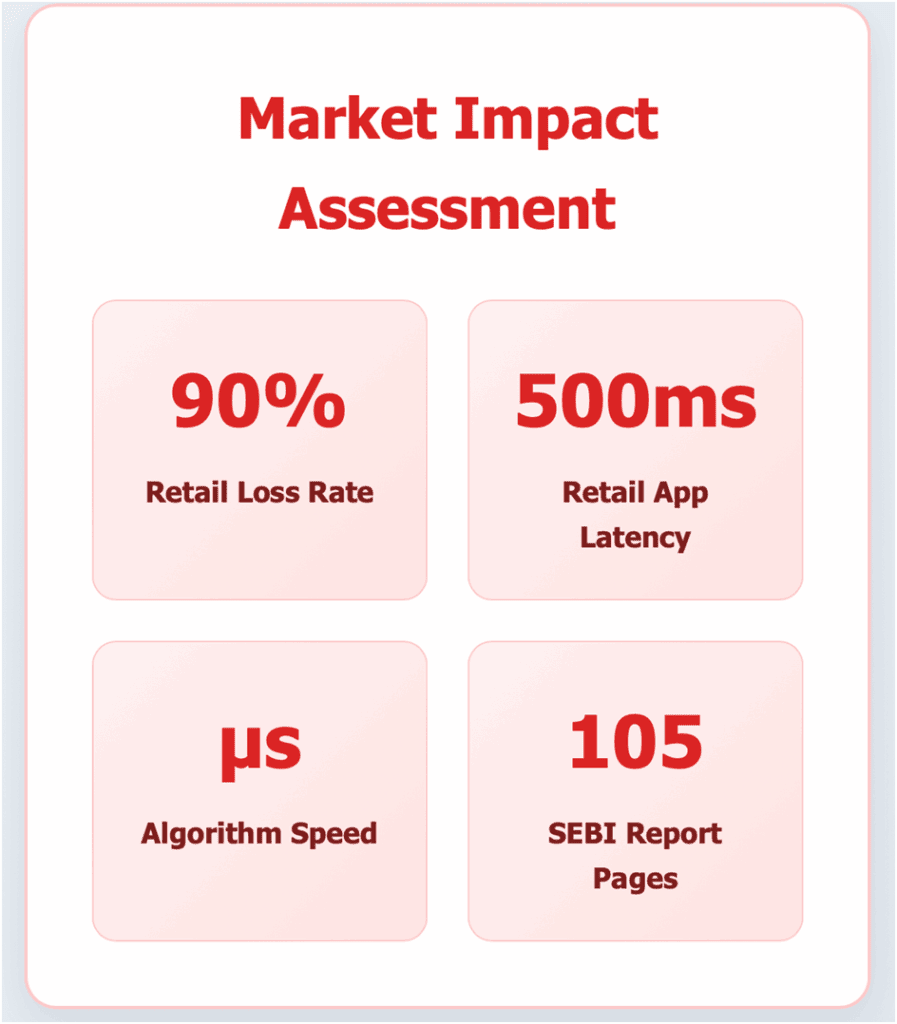

SEBI’s recent 105-page order outlines how Jane Street allegedly ran a ₹36,000 crore ($4.3 billion) strategy across multiple Bank Nifty expiry days. This wasn’t about taking directional bets. It was about moving the market itself, deliberately, strategically, and repeatedly.

Every Thursday morning, Jane Street’s algorithms would buy massive quantities of select banking stocks and index futures. This created an artificial rally in the Bank Nifty index, sometimes pushing it up by over 1,000 points. The timing wasn’t random. Between 9:15 AM and noon, retail interest typically spikes. As expected, thousands of retail traders began chasing the move, buying weekly call options at inflated premiums.

What most didn’t know is that Jane Street had already shorted those same call options. And as soon as sentiment reached its peak, the algo flipped. The firm began unloading its positions, triggering a sharp reversal. Within hours, the Bank Nifty would collapse, and the call options held by retail traders would expire worthless. Jane Street, meanwhile, walked away with extraordinary profits.

On January 17, 2024, they allegedly made ₹735 crores ($88 million) in a single day using this method.

How the Algorithm Worked: Speed, Scale, and Human Psychology

This wasn’t high-frequency trading in the traditional sense. It was behavioural manipulation powered by code.

Jane Street’s systems were co-located right next to exchange servers, allowing them to trade in microseconds. That means before a retail trader could even click ‘confirm,’ their order was already being priced in. But more than speed, it was their understanding of human behaviour that made the strategy lethal.

They knew exactly when retail traders were likely to chase a move. They knew how much volume was needed to tip sentiment. They understood how thinly traded banking stocks could be used to nudge the broader index. The game wasn’t to respond to the market, it was to create a setup that felt organic, lure in reactive traders, and then reverse the position to maximize the damage.

SEBI even noted that their trades were “sharp, large, and aggressive,” aimed at creating a “false or misleading appearance of market activity.” That’s a polite way of saying: these weren’t trades, they were traps.

Microstructure Red Flags: On several expiry days, order book imbalances and shallow depth in illiquid banking stocks exaggerated index movements. The VWAP (Volume Weighted Average Price) diverged significantly from settlement prices particularly during the final 30 minutes of trading suggesting tactical “marking the close” activity. Spread widening, followed by rapid liquidity pulls, further hinted at algo-driven manipulation designed to bait and exit before detection.

Why India? The Perfect Terrain for Predictable Chaos

To understand how this worked, you need to see what India’s options market has become. It’s the world’s biggest derivatives casino, and that’s not an exaggeration.

Young Indians are piling into weekly options like they’re buying lottery tickets. They believe they can turn ₹100 into ₹200 in minutes. Social media is full of influencers promising “guaranteed” strategies and easy money.

The numbers don’t lie: 90% of retail options traders lose money. Yet more people keep joining every day. Daily trading volume hit $3 trillion in just five years.

The psychology is simple. Show someone they can double their money quickly, and logic goes out the window. The exchanges make money on every trade. The brokers earn commissions. The influencers sell courses. Everyone profits except the actual traders.

Computers vs. Humans: No Contest

Here’s what makes me angry about this situation. Jane Street wasn’t just faster than retail traders, they were exploiting how people naturally behave under pressure.

Picture this: You’re a young professional in Mumbai with ₹50,000 in your trading account. You see Bank Nifty rising fast in the morning. Your trading groups are talking about easy profits. You buy call options. Then the index suddenly reverses in the afternoon, and your options expire worthless.

You think it’s bad luck or normal market movement. What you don’t know is that algorithms just played you. These systems can:

- Execute thousands of trades in milliseconds

- Analyze patterns humans can’t see

- Coordinate massive positions across different markets simultaneously

- Predict exactly how retail traders will react to fake price movements

Jane Street employs some of the smartest mathematicians in the world. They earn millions per year. They’re not competing against retail traders,they’re hunting them.

But This Isn’t Arbitrage. This Is Exploitation

Jane Street’s defense is familiar: they were performing “index arbitrage.” Aligning derivatives with the spot market. In theory, that’s a legitimate function.

But here’s the test, posed by rival quant Alexander Gerko: If your strategy is clean, it should work even with 1/100th the volume. If it only works when you can move the market, then it’s not arbitrage. It’s manipulation by size.

In this case, SEBI seems to agree. Their order points to repeated “marking the close” tactics where Jane Street pushed prices downward in the final hour of trade to profit from puts or short calls. These aren’t rare misfires. They’re structured, repeated behaviors.

The Counterpoint: What Jane Street Might Say

It’s only fair to acknowledge that Jane Street may argue their strategies complied with existing rules, and that their trades were within allowed limits on position size, margin, and timing.

They might argue that:

- They never prevented others from trading; retail traders made voluntary decisions.

- Market-making, arbitrage, and index adjustment are all legal strategies.

- Their actions, if impactful, were merely due to scale—not intent.

That’s where the legal gray zone lies. In markets driven by speed and size, intent becomes hard to prove until patterns emerge, as SEBI’s detailed forensic audit appears to show.

Retail Is Losing More Than Money, They’re Losing Trust

The tragedy here isn’t just the money lost. It’s the erosion of faith. Retail traders aren’t stupid. They’re just outmatched. They’re trading on phones with a half-second delay, against firms that model their emotional reactions and pre-position against them. They think they’re following momentum. But they’re being led into traps.

This is where the system truly fails. Brokers earn on churn. Influencers sell dreams. Exchanges reward volume. And the entire machine keeps spinning, until someone blows up, or a regulator steps in.

SEBI’s action against Jane Street is commendable. Freezing ₹4,700 crores, banning operations, and proposing reforms like fewer expiries and higher contract sizes is a step forward. But the underlying structure remains.

As long as behavioural volatility is profitable, someone will step in to exploit it.

Final Word: This Wasn’t Trading. This Was Hunting

Let’s not romanticize it. This wasn’t smart risk-taking or bold market-making. This was an algorithm engineered to trigger human error, amplified through scale, and monetized by speed.

It should be a wake-up call, for regulators, platforms, and traders alike. Because when financial markets start rewarding the ability to manipulate behaviours, the question isn’t who wins. It’s how much trust we lose in the system designed to protect us.

And trust, once gone, doesn’t return in microseconds.